Direct answer

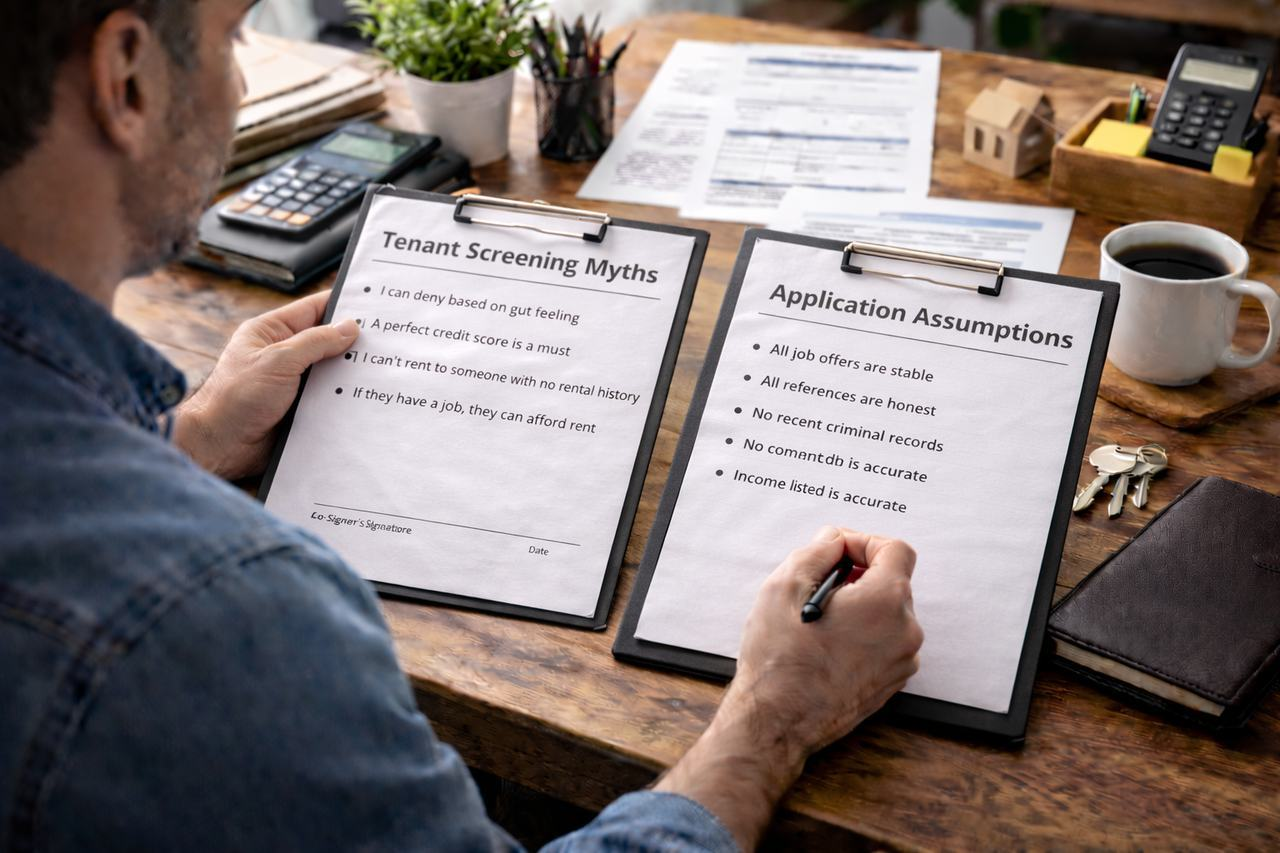

What should I know about Tenant Screening Myths?

Tenant Screening Myths helps rental owners make a clearer decision about leasing, tenant screening, cash flow, risk and long-term property performance. The best answer depends on the property, local demand, rent readiness, owner goals, legal requirements and the cost of vacancy or mistakes.

Myth 1: Credit score is the most important factor

Credit is only one part of screening. It reflects financial behavior, not affordability or tenancy performance.

Income stability and rental history often provide stronger insight into whether a tenant can and will pay rent consistently.

For a structured comparison, see credit vs income vs rental history.

Myth 2: Screening faster is always better

Fast screening feels efficient, but rushing decisions increases risk. Missing verification steps often causes more problems than slow screening.

A consistent process that balances speed and verification produces better outcomes.

Learn more in how long should tenant screening take.

Myth 3: Gut instinct is a good screening tool

Personal impressions are unreliable and create fair housing risk. Screening decisions should never be based on feelings or perceived trustworthiness.

Objective, written criteria protect landlords and applicants alike.

See why screening consistency matters.

Myth 4: Pay stubs and bank statements are always accurate

Altered or fabricated documents are more common than many landlords expect. Verifying consistency across documents is critical.

For verification techniques, review how to verify tenant income and documents and how to spot fake or forged tenant application documents.

Myth 5: A co signer fixes most screening issues

Co signers can reduce risk in limited situations, but they are not a cure all. They should never be used to offset major disqualifiers.

Clear standards matter.

For guidance, see when to accept a co signer.

Myth 6: Section 8 applicants cannot be screened

Applicants who use housing vouchers can and should be screened using lawful, consistent criteria. Voucher participation does not eliminate screening requirements.

What matters is applying the same standards to all applicants.

Learn more in screening Section 8 applicants.

Myth 7: Denying an application automatically creates legal risk

Denials themselves are not the problem. Inconsistent or undocumented denials create risk.

When decisions align with written criteria and proper notice is provided, denials are defensible.

For step by step guidance, see how to deny a rental application legally.

Myth 8: Adverse action notices are optional

When a decision is based on a consumer report, adverse action notices are often required. Failing to provide them is a common source of complaints and lawsuits.

Learn when they apply in adverse action notice explained.

Myth 9: Lawsuits only happen to large landlords

Screening related lawsuits affect landlords of all sizes. Smaller landlords may actually face greater risk due to informal or inconsistent processes.

For risk education, see tenant screening lawsuits explained.

Myth 10: Screening rules can change based on the situation

Changing standards based on vacancy pressure, personal circumstances, or applicant communication creates compliance risk.

Rules should be written once and applied consistently.

For the foundation of compliant screening, review rental application best practices and fair housing screening rules.

Using systems to avoid common mistakes

Screening software helps remove subjectivity, enforce criteria, and document decisions consistently.

Our property management software guide explains how technology supports better screening outcomes.

Final thoughts

Most tenant screening myths persist because they feel intuitive. A disciplined, documented process grounded in objective criteria leads to better tenants, fewer disputes, and lower long term risk.

Frequently asked questions

What should owners know about Tenant Screening Myths?

Tenant Screening Myths should be evaluated as a practical operating decision, not just a one-time task. Small process gaps can affect vacancy, risk and cash flow.

When should a landlord ask for help?

A landlord should ask for help when vacancy, screening, maintenance coordination, legal notices or decision fatigue start affecting the property’s performance.

What is the next step?

The next step is to compare the current rental process against a documented management or leasing plan and identify the highest-cost bottleneck.