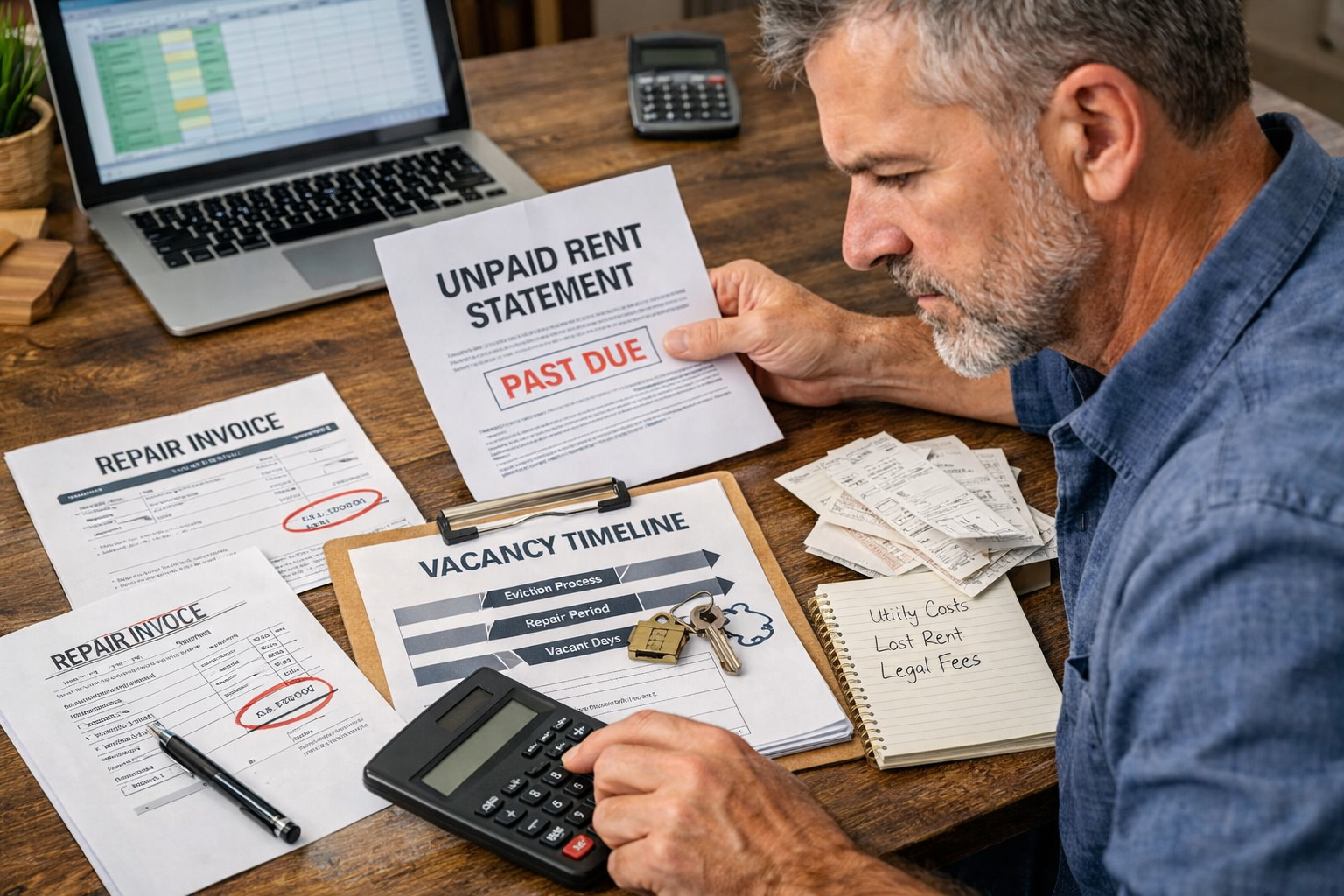

What Does One Bad Tenant Really Cost?

Answer: Usually far more than the security deposit covers.

A bad tenant rarely costs just one month of rent. The real impact comes from compounding losses across vacancy, damage, legal exposure, and time. This tool helps you quantify the full financial picture so you can price risk correctly, screen properly, and build reserves that reflect reality. For a broader view of how tenant risk affects overall property performance, review our Rental Property Cash Flow hub.

Why Landlords Underestimate This

Most landlords mentally calculate loss like this:

“They skipped one month of rent.”

But the true cost stack often includes:

- Two to three months of non payment

- Legal filings or negotiated cash for keys

- Extended vacancy during turnover

- Property damage beyond normal wear

- Discounted rent to fill quickly

- Your own time and stress

When stacked together, one bad tenant can wipe out an entire year of profit. That is exactly why landlords need to understand not just the event cost, but the ongoing effect on rental property cash flow.

Bad Tenant Cost Calculator Framework

Work through each category honestly. Most losses fall into five buckets.

1. Lost Rent

- Months unpaid

- Partial payments

- Concessions to regain possession

Example: $1,500 rent × 3 months = $4,500

2. Vacancy Loss After Move Out

- Days to clean and repair

- Days to market

- Days to place and collect first rent

Example: 45 days vacancy at $1,500 monthly = $2,250

3. Damage and Make Ready

- Trash out and deep cleaning

- Flooring replacement

- Paint beyond standard turnover

- Appliance repair

- Plumbing issues

Example: $6,000 in repairs

4. Legal and Administrative Costs

- Eviction filing fees

- Attorney fees

- Court costs

- Utility carrying costs during vacancy

Example: $1,200 to $3,000 depending on complexity

5. Hidden Opportunity Cost

- Time you could have spent leasing faster

- Emotional fatigue leading to poor next screening

- Deferred maintenance compounding later

These hidden losses matter because one bad tenant can distort the property’s performance for months, sometimes longer. If you want to evaluate the bigger financial picture beyond this single event, use the Rental Property Cash Flow hub.

Realistic Total Example

Lost rent: $4,500

Vacancy loss: $2,250

Damage: $6,000

Legal and utilities: $2,000

Total: $14,750

If your annual net cash flow is $4,000, that single tenant erased nearly four years of profit. That is why tenant quality and reserve planning should be tied directly to your rental property cash flow assumptions.

Stress Test Questions

- Could your reserves absorb a $10,000 shock?

- Would that force you to use personal savings?

- Would it push you to sell prematurely?

- Would it make you rush the next tenant decision?

If the answer to any of those is yes, your reserve structure may not match your risk exposure. It may also mean your property’s true cash flow profile is weaker than it appears during smooth months.

How to Reduce the Probability

- Raise screening standards

- Verify income rigorously

- Do not lower criteria for urgency

- Build 3 to 6 months of operating reserves

- Price rent appropriately for tenant quality

In other words, the goal is not just avoiding bad tenants. The goal is protecting consistent rental property cash flow over time.

Related Landlord Decision Tools

- Landlord Decision Tools Hub

- Rental Property Cash Flow

- Is My Rental Still Worth Keeping

- Should I Sell or Keep My Rental Property

- How Much Risk Can I Afford as a Landlord

- Raising Rent vs Re Leasing a Property

Bottom Line

One bad tenant is not just an inconvenience. It is a capital event.

If your systems, reserves, and screening standards cannot withstand that event, the issue is not luck. It is structure.

Use this clarity to build a rental portfolio that survives mistakes without destabilizing your life. Then step back and evaluate whether the property still works through the lens of long term Rental Property Cash Flow.